Our Home Renovation Loan Diaries

Our Home Renovation Loan Diaries

Blog Article

The Ultimate Guide To Home Renovation Loan

Table of ContentsThe smart Trick of Home Renovation Loan That Nobody is Talking AboutHow Home Renovation Loan can Save You Time, Stress, and Money.The smart Trick of Home Renovation Loan That Nobody is Discussing8 Easy Facts About Home Renovation Loan ExplainedHome Renovation Loan for Dummies

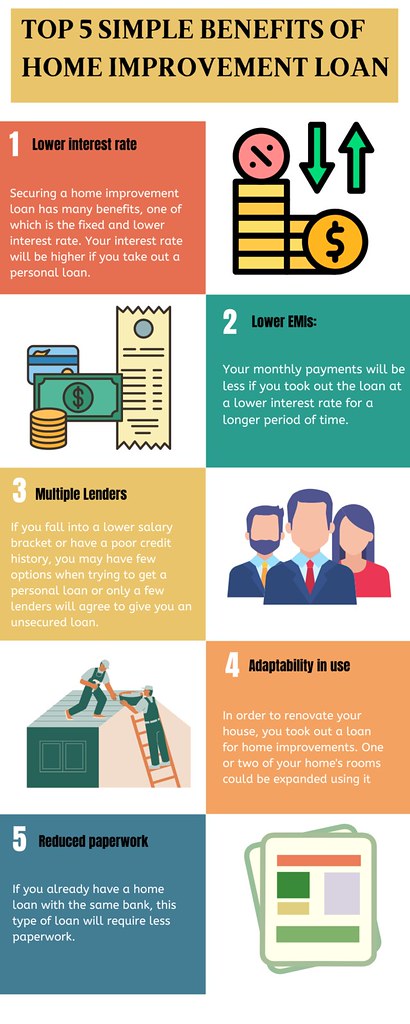

Presume you additionally think about the decreased interest price on this funding. Take into consideration a house restoration funding if you desire to remodel your home and give it a fresh look. Banks give finances for homeowners that desire to renovate or improve their homes but need the money. With the help of these financings, you may make your home a lot more cosmetically pleasing and comfortable to live in.There are plenty of funding choices offered to assist with your home improvement. The appropriate one for you will rely on how much you need to obtain and exactly how swiftly you wish to pay it off. Brent Differ, Branch Manager at Assiniboine Cooperative credit union, provides some practical guidance. "The first point you should do is get quotes from several specialists, so you know the reasonable market price of the job you're obtaining done.

The main benefits of using a HELOC for a home remodelling is the flexibility and low rates (generally 1% above the prime price). Furthermore, you will only pay interest on the quantity you withdraw, making this a good alternative if you require to pay for your home renovations in phases.

The major downside of a HELOC is that there is no fixed repayment timetable. You have to pay a minimum of the interest monthly and this will certainly boost if prime rates go up." This is an excellent financing option for home restorations if you intend to make smaller sized regular monthly repayments.

Excitement About Home Renovation Loan

Provided the possibly long amortization duration, you can end up paying substantially more passion with a mortgage refinance compared to other financing alternatives, and the costs linked with a HELOC will likewise use. home renovation loan. A mortgage refinance is effectively a brand-new home mortgage, and the rates of interest might be more than your present one

Prices and set-up expenses are typically the like would certainly pay for a HELOC and you can settle the financing early without any charge. Some of our consumers will start their restorations with a HELOC and after that switch over to a home equity lending once all the costs are validated." This can be a great home restoration financing choice for medium-sized projects.

Personal car loan rates are generally higher than with HELOCs typically, prime plus 3%., the main disadvantage is the passion rate can generally range in between 12% to 20%, so you'll desire to pay the balance off quickly.

Home improvement lendings are the financing choice that permits home owners to refurbish their homes without having to dip into their financial savings or splurge on high-interest credit score cards. There are a range of home remodelling loan resources offered to select from: Home Equity Credit Line (HELOC) Home Equity Loan Home Mortgage Refinance Personal Funding Credit History Card Each of these financing choices comes with unique requirements, like credit history, owner's earnings, credit line, and rate of interest prices.

All about Home Renovation Loan

Prior to you start of designing your dream home, you most likely would like to know the a number of kinds of home improvement fundings readily available in copyright. Below are some of the most common kinds official statement of home remodelling finances each with its very own collection of characteristics and benefits. It is a kind of home enhancement finance that permits homeowners to borrow an abundant sum of money at a low-interest rate.

These are advantageous for massive restoration jobs and have lower rate of interest than other types of personal car loans. A HELOC investigate this site Home Equity Line of Credit history resembles a home equity lending that utilizes the value of your home as security. It works as a bank card, where you can borrow based on your demands to fund your home remodelling projects.

To be qualified, you have to have either a minimum of a minimum of 20% home equity or if you have a mortgage of 35% home equity for a standalone HELOC. Re-financing your home mortgage process involves changing your present home loan with a new one at a reduced price. It decreases your monthly settlements and lowers the amount of rate of interest you pay over your lifetime.

The 9-Minute Rule for Home Renovation Loan

For this, you might need to offer a clear construction plan and spending plan for the renovation, consisting of calculating the price for all the materials needed. Additionally, personal car loans can be protected or unprotected with much shorter repayment durations (under 60 months) and included a greater rates of interest, relying on your credit report rating and revenue.

Things about Home Renovation Loan

Store funding programs, i.e. Store debt cards are used by many home enhancement stores in copyright, such as Home Depot or Lowe's. If you're preparing for small home enhancement or do it yourself jobs, such as mounting new home windows or bathroom restoration, getting a store card via the seller can be a very easy and quick process.

Report this page